The idea of a mobile wallet has been touted as the next big thing for years now, and despite pioneering trials from the likes of Nokia (that, among other things, enabled users to pay for vending machine items via text messages), the technology hasn’t changed the lives of many consumers. That may be changing, as companies like Visa and MasterCard start to put their muscle behind mobile payment technologies, and firms like Google begin offering tools like the NFC-enabled Google Wallet. Now the disruptive mobile payment startup Square is upping its game, announcing a new version of its Card Case mobile payment solution. How does Card Case work, and how does it compare to other mobile payment systems?

Inside Square’s Card Case

Inside Square’s Card Case

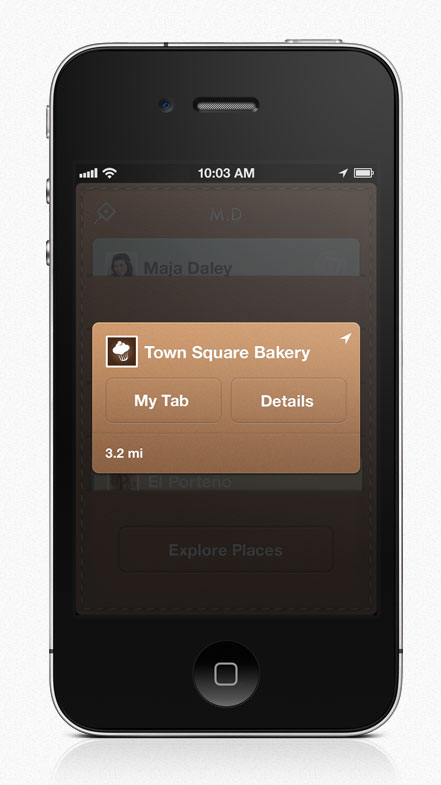

Square’s Card Case enables users to pay for purchases at merchants and businesses they frequent regularly — relying on clerks, waitstaff, and business managers to recognize their regular patrons. Users link their credit cards to the Card Case app on their iOS or Android device. When they visit a merchant that’s Card Case-enabled, they use the Card Case app to open their tab. (The latest version of Card Case can open tabs automatically when a user gets within 100 meters of a merchant they like.) When users are ready to go, they just walk up to the clerk or cashier and give their name: The business’s Card Case app already shows the customer is in the store, and the cashier can verify the purchases and the user’s identity thanks to a photo of the user that pops up along with the transaction. If everything is kosher, the merchant just presses the transaction button, and the purchase goes through. Square later sends the customer a receipt. No cards, no swiping, no bumping cellphones to terminals, no signatures. If the user has opted to let tabs open automatically based on location, they don’t even have to take their phone out of their pocket.

Square looks at Card Case as a way to make the purchasing experience more transparent for customers. That’s basically business-speak for removing barriers that inhibit consumers from spontaneously spending money. Square also encourages spur-of-the-moment purchasing within the app by enabling users to pull up lists of featured and nearby Card Case-enabled merchants, making it easier for folks to find places where Card Case can work for them. Square is also offering benefits to merchants: When customers use Card Case, they can get loyalty cards for businesses that include not just contact information, but a wealth of other details about the business, including click-to-call capability, images, menus, and even direct integration with Twitter so users can see comments and social media interactions with customers. Square takes a 2.75 percent cut of every transaction.

Of course, the trick to Card Case might be finding Card Case-savvy merchants. Square says more than 20,000 merchants have signed up for the service since it launched in August, and the company expects the new hands-free payment capabilities will bring more merchants (and customers) on board.

How Card Case stacks up to Google Wallet

Square’s Card Case’s unique spin on mobile payments market is location information. It allows Square to know when a customer is near a Card Case-enabled business, then open their tab automatically — the technique is called “geo-fencing.” Geo-fencing relies on GPS and assisted GPS technology to get a fix on a user’s location and compare that to the known locations of Card Case-enabled businesses. The idea is that Card Case doesn’t work unless a user has deliberately set up a tab for a Card Case-enabled business, and a transaction won’t go through unless the merchant recognizes the buyer— or is at least satisfied the person in front of them is a close-enough match to the profile photo displayed by Card Case.

There is, of course, the possibility a user might have multiple tabs set up for Card Case-enabled businesses within 100m of each other. Think food courts, street fairs, and shopping malls. That leaves plenty of room for customer and (especially) merchant confusion if Card Case were to become ubiquitous. And, just like the rest of Square’s transaction processing, the burden is on the merchant to submit only valid transactions. Square is confident that even without signatures or physical card swipes, it can stave off consumer fraud.

Card Case requires no special hardware: it runs on existing iOS devices (iPads, iPhones, and iPod touches) running iOS 4.1 or later, or phones and other devices running Android 2.1 or later.

Card Case’s design is a stark contrast to Google Wallet, which operates in a manner much closer to traditional credit card. Where Square’s Card Case can open a connection to a merchant just by getting within 100 meters of them, Google Wallet operates via Near Field Communication (NFC) with secured point of sale devices that merchants purchase or lease from payment processors. NFC transactions only work with devices that are within a few inches of each other, meaning users have to hold their phones or other devices quite close to the point-of-sale terminal to get their transaction to go through. And NFC hardware isn’t the only thing Google Wallet requires: Users also need a device with Secure Element support. Basically, a Secure Element is a separate hardware subsystem within the phone that’s separated from the phone’s operating system and applications for security. Even if, say, there were some major zero-day security gaffe that exposed everything in an Android device to the entire world, data stored in the Secure Element system wouldn’t be compromised. The Secure Element stores user’s account details, and only permits access to them from authorized programs that meet multiple security requirements.

Right now, the only phone on the market that supports Google Wallet is the Nexus S 4G on Sprint, and Google Wallet can only be used with NFC terminals that support MasterCard PayPass. Users also need either a Citi MasterCard or a Google PrePaid Card (which, in turn, is backed by MasterCard and Money Network). Many handset vendors have promised support for NFC payment technology and Google promises it is working to bring a vast number of other card issuers on board. so that everything from other credit cards to merchant loyalty cards can all be handled via Google Wallet—time will tell whether Google can deliver on those promises. But, for now, Google Wallet is a pretty limited case.

However, Google Wallet may have one advantage over Square’s Card Case. It does not require customers to set up a “tab” or account for a merchant using an app on their device before they can carry out a transaction. Instead, users can use their phones at participating NFC merchants without having to configure anything in their devices, or worry about whether they’re enough GPS and location information is available to make them eligible for hands-free buying. Just get their phone near a terminal, and it’s done.

In both cases, users will need to make sure their phones are charges and activated to carry out transactions. In a world of mobile transactions, a dead battery may literally make people penniless.

The Apple Store App

The iPhone 4S famously doesn’t include NFC technology, so there’s no way it’s going to be participating in Google Wallet — and, despite many rumors, there’s no word whether future iPhones will adopt NFC and Secure Element technology.

However, that doesn’t mean Apple is steering clear of mobile payment solutions. Apple is widely expected to launch an Apple Store app for iOS devices this week. Among other things, the app will enable users to place orders for pickup through their local Apple Store, and — perhaps most significantly — enable self-checkout at Apple Stores. (Many unattributed details are available via Boy Genius Report and other outlets.) Order pickup isn’t terribly revolutionary, but will undoubtedly ease some users’ frustration trying to make purchases at some Apple Stores that often resemble zoos. Reports have Apple promising a 12-minute turnaround from when a customer places an order for in-stock items and when they’ll be available for pickup. At least initially, the service will only be available in the United States.

The reported self-checkout capability is perhaps the most intriguing: Users would locate the item they want in the store, say an iPhone accessory, then take a photo of the purchase using their device (presumably via a barcode or QR code). Once confirmed, the purchase will automatically be made to the same credit card associated with an Apple ID, which is likely the same credit card customers use to purchase through iTunes or the Mac App Store. Then users can just walk out the door. Of course, if users want to pay via another card or use cash, they won’t be able to use the self-checkout option.

Apple’s in-store app isn’t a generalized solution like Google Wallet or Square’s Card Case — it’ll only work at Apple Stores. However, it does have a chance to set the bar for how everyday consumers expect mobile payments to work. After all, millions of Americans have iOS devices, and millions of those people visit Apple Stores. If Apple can make self-checkout work well in its retail stores, other businesses — and even mobile payment providers — will likely have to look at ways to offer the same convenience in their solutions.